The Frontier AI Scale-Up Problem

Why the UK and Europe Struggle to Scale and Retain Frontier AI Champions · Zoi Roupakia · July 2026

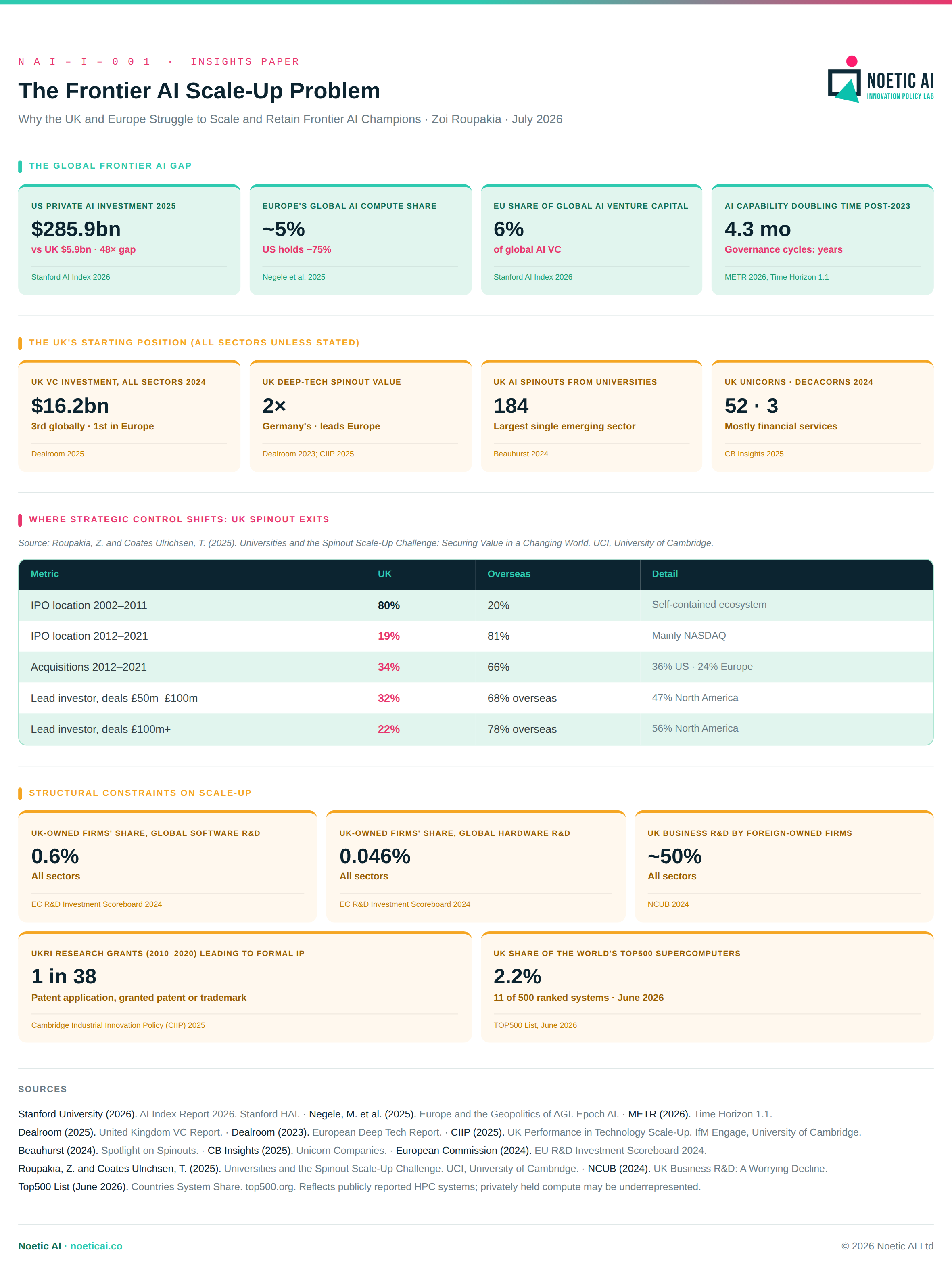

US private AI investment 2025

$285.9bn

vs UK $5.9bn · 48× gap

Stanford AI Index 2026

Europe's global AI compute share

~5%

US holds ~75%

Negele et al. 2025

EU share of global AI venture capital

6%

of global AI VC

Stanford AI Index 2026

AI capability doubling time post-2023

4.3 mo

Governance cycles: years

METR 2026, Time Horizon 1.1

UK VC investment, all sectors 2024

$16.2bn

3rd globally · 1st in Europe

Dealroom 2025

UK deep-tech spinout value

2×

Germany's · leads Europe

Dealroom 2023; CIIP 2025

UK AI spinouts from universities

184

Largest single emerging sector

Beauhurst 2024

UK unicorns · decacorns 2024

52 · 3

Mostly financial services

CB Insights 2025

Source: Roupakia, Z. and Coates Ulrichsen, T. (2025). Universities and the Spinout Scale-Up Challenge: Securing Value in a Changing World. UCI, University of Cambridge.

| Metric | UK | Overseas | Detail |

|---|---|---|---|

| IPO location 2002–2011 | 80% | 20% | Self-contained ecosystem |

| IPO location 2012–2021 | 19% | 81% | Mainly NASDAQ |

| Acquisitions 2012–2021 | 34% | 66% | 36% US · 24% Europe |

| Lead investor, deals £50m–£100m | 32% | 68% overseas | 47% North America |

| Lead investor, deals £100m+ | 22% | 78% overseas | 56% North America |

UK-owned firms' share, global software R&D

0.6%

All sectors

EC R&D Investment Scoreboard 2024

UK-owned firms' share, global hardware R&D

0.046%

All sectors

EC R&D Investment Scoreboard 2024

UK business R&D by foreign-owned firms

~50%

All sectors

NCUB 2024

UKRI research grants (2010–2020) leading to formal IP

1 in 38

Patent application, granted patent or trademark

Cambridge Industrial Innovation Policy (CIIP) 2025

UK share of the world's Top500 supercomputers

2.2%

11 of 500 ranked systems · June 2026

TOP500 List, June 2026

Sources

- Stanford University (2026). AI Index Report 2026. Stanford Human-Centered Artificial Intelligence (HAI). Note: $285.9bn is private AI investment; distinct from AI chip-market data.

- Negele, M., Fietta, L., Koessler, L., van der Burgt, N., Anderljung, M., et al. (2025). Europe and the Geopolitics of AGI: The Need for a Preparedness Plan. Epoch AI / Ellis Institute.

- METR (2026). Time Horizon 1.1: Measuring AI Ability to Complete Long Tasks. Model Evaluation and Threat Research.

- Dealroom (2025). United Kingdom: Venture Capital and Technology Report.

- Dealroom (2023). The 2023 European Deep Tech Report.

- Cambridge Industrial Innovation Policy (2025). UK Performance in Technology Scale-Up. IfM Engage, University of Cambridge.

- Beauhurst (2024). Spotlight on Spinouts April 2024: UK Academic Spinout Trends.

- CB Insights (2025). The Complete List of Unicorn Companies.

- Roupakia, Z. and Coates Ulrichsen, T. (2025). Universities and the Spinout Scale-Up Challenge: Securing Value in a Changing World. Policy Evidence Unit for University Commercialisation and Innovation (UCI), Institute for Manufacturing, University of Cambridge. Apollo Repository.

- European Commission (2024). EU Industrial R&D Investment Scoreboard 2024. Joint Research Centre, European Commission.

- NCUB (2024). UK Business R&D: A Worrying Decline. National Centre for Universities and Business.

- Top500 List (June 2026). Countries System Share. top500.org. Reflects publicly reported HPC systems; privately held compute may be underrepresented.

Download the full infographic

Downloads as NAI-I-001_infographic.png

{kind=link}

Prototype visualisation. Content and functionality may be refined as the evidence base develops.